TL;DR:

- Fintech success depends on understanding financial logic and compliance before development starts.

- AI and blockchain are powerful when used with purpose-built models and integrated into hybrid architectures.

- Choosing specialized, experienced fintech partners accelerates deployment and reduces costly rework.

Fintech success stories rarely come down to which framework your engineers know best. They come down to whether your team understood the financial logic, mapped the compliance requirements, and chose the right technology architecture before a single line of code was written. Most companies skip those steps and pay for it later, through rework, regulatory delays, and products that fail to scale. This guide breaks down what modern fintech software development actually requires, how AI and blockchain function as genuine business engines rather than buzzwords, and how to make strategic decisions that protect your investment from day one.

Table of Contents

- The new reality: Fintech software is more than coding

- AI and blockchain: The engines of scalable fintech

- Choosing the right fintech development partner

- Best practices for fintech software implementation

- What most guides miss: The real hidden costs and leverage in fintech dev

- Unlock your fintech solution with expert partners

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Go beyond just coding | Fintech projects succeed through smart financial logic, compliance, and risk management. |

| Leverage specialized AI and blockchain | Purpose-built AI models and hybrid blockchain integrations drive scalable, trusted automation. |

| Choose expert development partners | Specialized teams reduce time-to-launch and integration rework, saving costs and ensuring compliance. |

| Follow privacy and regulatory best practices | Protect user data with PII masking and federated learning, and always include human-in-the-loop for high-risk tasks. |

| Watch for hidden costs | Generic dev teams may lead to costly rework; specialized partners unlock faster ROI. |

The new reality: Fintech software is more than coding

There is a persistent belief in many boardrooms and startup pitch decks that fintech development is primarily an engineering challenge. Get the right developers, pick a technology stack, and build fast. That belief is one of the most expensive mistakes a company can make.

"Fintech is not 'just coding'—success hinges on financial logic, regulatory design, risk trade-offs before implementation; poor scoping leads to failures."

Financial logic comes first. Every fintech product, whether a lending platform, payment gateway, trading tool, or insurance app, must model real financial behavior accurately. Interest calculations, settlement timing, currency conversion rules, and fee structures are not simple formulas. They change by jurisdiction, product type, and regulatory environment. When these rules are misunderstood at the outset, the resulting software fails in production and often in audits.

Compliance design is not an afterthought. Regulations like PSD2 in Europe, ADGM frameworks in the UAE, and FinCEN requirements in the United States are baked into every transaction flow. Building a product and then retrofitting compliance is extraordinarily expensive. It is the equivalent of constructing a building and then trying to add fire exits after occupants move in.

Here is what the pre-development phase of a serious fintech project must address:

- Jurisdiction mapping: Which regulatory bodies govern your users, merchants, and financial flows?

- Risk classification: What financial risks does the product create and how will they be mitigated by design?

- Data governance: What user financial data is collected, stored, and processed, and under which privacy frameworks?

- Failure mode analysis: What happens when a transaction fails, a third-party API is unavailable, or a fraud case is detected?

- Audit trail architecture: How will the system prove compliance to regulators retroactively?

Organizations that invest time here build scalable enterprise solutions that survive regulatory scrutiny. Organizations that skip it build technical debt at enterprise scale.

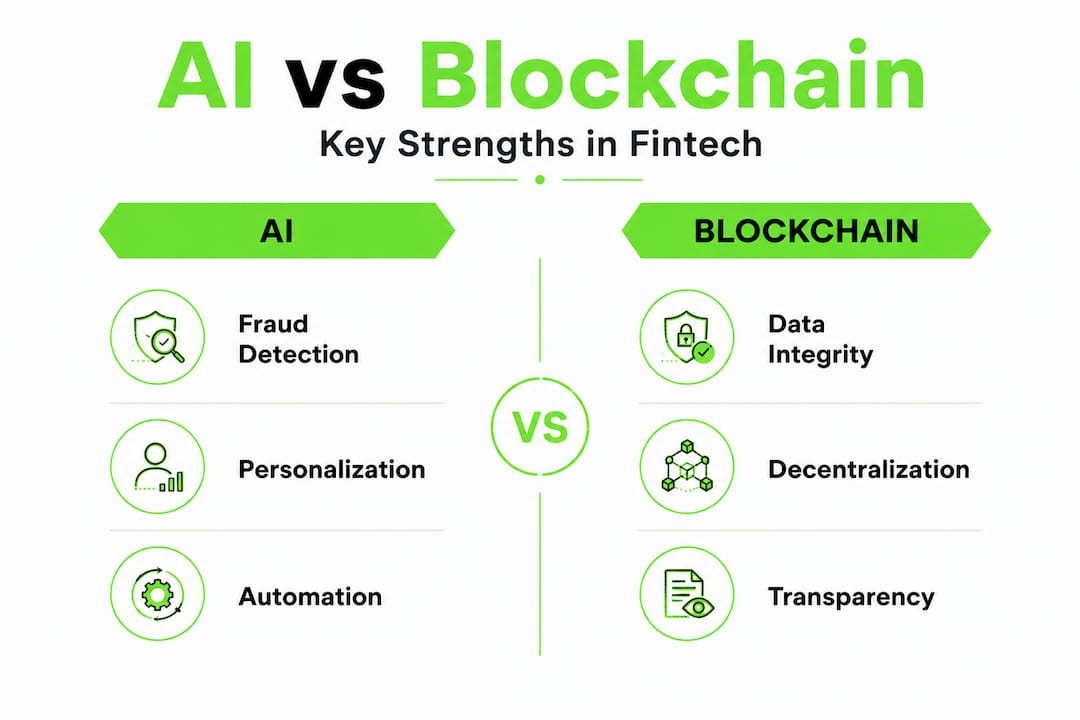

AI and blockchain: The engines of scalable fintech

Once the strategic and compliance foundation is set, the technology choices become clearer and far more powerful. AI and blockchain are not interchangeable add-ons. They solve distinct problems, and they are most effective when deployed with precision.

How AI is transforming fintech operations

Large language models (LLMs) have opened significant new possibilities in financial services. Fraud detection systems can now process natural language transaction descriptions, flag contextual anomalies, and generate human-readable explanations for compliance teams. Robo-advisors powered by LLMs can engage clients in plain-language conversations about portfolio risk, investment options, and tax implications. Personalization engines can recommend relevant financial products based on spending behavior and life stage.

However, there is a critical distinction that many technology leaders overlook. General LLMs cap at 66% accuracy in transaction classification tasks, while specialized, purpose-built AI models reach 93% accuracy for the same tasks. That gap is enormous in a financial context. A 7% misclassification rate on credit risk decisions or fraud flags is acceptable in no regulatory environment.

This finding has direct implications for how you architect your AI stack. A general LLM can serve as a user-facing conversational layer or a document summarization tool. For transaction classification, anomaly detection, and credit scoring, you need models trained on domain-specific financial data with rigorous validation.

| AI use case | General LLM performance | Specialized model performance | Recommended approach |

|---|---|---|---|

| Transaction classification | 66% accuracy | 93% accuracy | Specialized model required |

| Fraud detection narrative | High | Medium | LLM with human review |

| Client personalization | High | High | LLM suitable |

| Robo-advisory conversations | High | Medium | LLM with compliance guardrails |

| Credit risk scoring | Low | Very high | Specialized model only |

Pro Tip: Before choosing an AI vendor or model, run a benchmark test on a sample of your actual transaction data. The performance difference between a general model and a specialized one will be obvious, and it will save you from building a system that underperforms at scale.

Why blockchain belongs in your fintech architecture

Blockchain's core value in fintech is trust without a central authority. For multi-party financial flows such as trade finance, cross-border remittance, and tokenized assets, blockchain creates a shared, tamper-proof record that all participants can verify. This eliminates reconciliation delays, reduces counterparty risk, and makes audits dramatically simpler.

AI and blockchain scalability becomes genuinely powerful when both technologies are combined in a hybrid architecture. Smart contracts can automatically execute financial agreements when predefined conditions are met, while AI models monitor those conditions in real time. This is not theoretical. Payment clearing networks, insurance claims automation, and lending platforms are already running hybrid models.

That said, hybrid AI-blockchain systems require purpose-built models rather than general LLMs to function reliably. The immutability of blockchain means that decisions executed on-chain cannot easily be reversed. Errors in AI logic become permanent records. This is why the model architecture and testing regimen for on-chain AI logic must be extraordinarily rigorous.

If you are exploring AI agents for automation in your fintech stack, understand that the opportunity is real, but the architecture must be custom. Off-the-shelf solutions will not meet the precision requirements your financial use case demands. For teams exploring blockchain for startups, the earlier you design for on-chain logic, the easier integration becomes.

Choosing the right fintech development partner

Technology decisions are only as good as the team that implements them. The fintech development market is crowded, and the difference between a specialized partner and a general software agency often becomes visible only after months of costly work.

Specialized fintech partners consistently outperform general developers for one core reason: they have already solved the integration and compliance problems you are facing. They are not learning on your budget. This translates directly into delivery timelines of 12 to 16 weeks for projects that would take general development teams significantly longer, along with meaningfully lower total project cost due to fewer integration failures and compliance rework cycles.

Here is how to evaluate a fintech development partner before signing a contract:

- Ask for fintech-specific case studies. Not just software portfolios. Specifically financial services projects, including what regulatory environment they operated in and what compliance challenges they solved.

- Probe their pre-development process. Do they start with financial logic mapping and risk design? Or do they jump straight to architecture and sprints? The former signals fintech maturity.

- Evaluate their AI and blockchain credentials separately. A team strong in mobile development but inexperienced in smart contracts or AI model training will struggle with hybrid solutions.

- Ask about pre-built components. Reputable fintech partners maintain libraries of tested components for KYC flows, payment gateway integrations, and compliance reporting. These reduce your cost and timeline meaningfully.

- Assess their compliance knowledge by jurisdiction. If you operate in the UAE and EU, your partner must understand ADGM, DIFC, and GDPR frameworks by name and practice, not just in principle.

| Evaluation factor | General software agency | Specialized fintech partner |

|---|---|---|

| Compliance familiarity | Learned during your project | Pre-existing expertise |

| Integration speed | Slower, more rework | Faster, fewer errors |

| AI model capability | General purpose | Domain-specific options |

| Delivery timeline | Variable, often 6+ months | 12 to 16 weeks typical |

| Pre-built components | Unlikely | Available and tested |

A team with fintech development expertise will also maintain relationships with compliance consultants and financial regulators, which accelerates your go-to-market timeline in ways that raw engineering skill cannot replicate.

Best practices for fintech software implementation

Even with the right partner and the right technology, implementation choices determine whether your product succeeds. These practices reflect what high-performing fintech teams actually do, not just what is recommended in theory.

Protect user data from the design stage. Regulations in virtually every market require that personally identifiable information (PII) is never exposed to AI training pipelines without explicit safeguards. PII masking strips or transforms identifying information before it reaches any model. Federated learning goes further, allowing AI models to learn from distributed datasets held by different institutions without the raw data ever being centralized. Both techniques are now standard requirements rather than advanced options, as general LLMs require PII masking and federated learning for safe deployment in financial environments.

Keep humans in the loop for high-stakes decisions. AI can flag fraud, score credit risk, and recommend products at machine speed. But when those decisions affect real people's access to financial services, human review is both ethically important and increasingly required by regulators. Build your workflows so that high-risk decisions have mandatory human checkpoints before execution.

Treat compliance as a feature, not a constraint. The most successful fintech companies design their compliance workflows into the product user experience. KYC onboarding, AML monitoring, and transaction reporting are not back-office burdens. They are product features that your enterprise clients will evaluate before signing contracts.

Pro Tip: Build your audit trail architecture during the initial sprint, not after launch. The ability to produce a complete, timestamped record of every transaction, decision, and user action is frequently what separates products that pass regulatory review from those that do not.

Plan for scale from the first version. Microservices architecture, API-first design, and cloud-native infrastructure are not luxuries for phase two. Fintech platforms that start monolithic and try to scale often face complete rewrites at exactly the wrong moment, when user growth and regulatory attention are peaking. Prioritize AI-driven innovation practices that accommodate future model updates without architectural disruption.

What most guides miss: The real hidden costs and leverage in fintech dev

Most technology guides talk about upfront development costs and timelines. They miss the costs that accumulate quietly in the background: rework cycles from underspecified compliance requirements, late-stage integration failures with payment processors, regulatory fines from data handling errors, and the opportunity cost of delayed market entry.

From our experience building across the fintech, blockchain, and AI sectors, the most consistent finding is this: the teams that invest heavily in strategic planning before development start spending far less total. A six-week discovery phase focused on financial logic, regulatory mapping, and architecture design routinely prevents four to six months of expensive rework later.

The second thing most guides underestimate is the leverage that specialized teams provide in hybrid AI-blockchain environments. General advice says "use AI for fraud detection and blockchain for transparency." That is accurate but incomplete. The real leverage comes from purpose-built AI models making decisions that trigger smart contract execution automatically, creating fully automated financial workflows that require no human intervention for standard cases and escalate edge cases intelligently. Hybrid AI-blockchain architectures provide this kind of compounding efficiency, and the impact is particularly pronounced for smaller financial institutions in developing markets where operational costs are the primary constraint.

The Dubai blockchain-AI ecosystem is one of the most active proving grounds for these hybrid models precisely because the regulatory environment is progressive and the market demands real-world performance. What we see consistently is that companies using templated or off-the-shelf fintech solutions hit a ceiling. The ones that invest in custom architecture built around their specific financial logic and compliance environment scale past that ceiling without the structural rewrites their competitors face.

The uncomfortable truth is that fintech software development is expensive if done wrong and remarkably cost-effective if done right. The variable is almost always the quality and specialization of the team you choose at the beginning.

Unlock your fintech solution with expert partners

Ready to leverage these insights for your own fintech initiative?

Proud Lion Studios brings deep expertise in financial software, blockchain architecture, and AI model development to every client engagement. Whether you are building a payment platform, a tokenized asset marketplace, or an AI-powered lending product, our fully UAE-based technical team works from the ground up on your specific financial logic, compliance environment, and scalability requirements. Our blockchain development services and AI agents for fintech are built around real business outcomes, not templated packages. If you are ready to move from concept to a compliant, scalable fintech product, let us show you what specialized development actually looks like.

Frequently asked questions

What makes specialized fintech development teams better than generalists?

Specialized fintech partners reduce costly rework on compliance and integrations, delivering projects in 12 to 16 weeks with lower total cost than general agencies. Their domain expertise means they solve your problems using proven methods rather than discovering them at your expense.

How do AI and blockchain improve fintech software security and trust?

AI automates fraud detection and personalizes financial services at scale, while blockchain creates tamper-proof transaction records that satisfy audit and regulatory requirements. However, AI in transaction classification reaches its full potential only with specialized models, not general LLMs.

What is the role of PII masking and federated learning in fintech AI?

PII masking prevents sensitive financial data from being exposed during AI training, and federated learning allows models to improve from distributed institutional data without centralizing it. Together, they enable compliant AI deployment in regulated financial environments.

How does hybrid AI-blockchain impact fintech in emerging markets?

Hybrid AI-blockchain solutions have an outsized positive effect on smaller financial institutions in developing markets, where operational efficiency gains translate directly into competitive performance improvements. Purpose-built AI models, rather than general LLMs, are what make these architectures work reliably.